IC Insights IC Insights

IC Insights, Inc. is a leading semiconductor market research company headquartered in Scottsdale, Arizona, USA. Founded in 1997, IC Insights offers complete analysis of the integrated circuit (IC), optoelectronic, sensor/actuator, and discrete semiconductor markets with coverage including current … More » CMOS Image Sensor Sales Stay on Record-Breaking PaceMay 8th, 2018 by IC Insights

Embedded imaging applications in cars, security, machine vision, medical, virtual reality, and other new uses will offset slow growth in camera phones, says new report.

The spread of digital camera applications in vehicles, machine vision, human recognition and security systems, as well as for more powerful camera phones will drive CMOS image sensor sales to an eighth straight record-high level this year with worldwide revenues growing 10% to $13.7 billion, following a 19% surge in 2017, according to IC Insights’ 2018 O-S-D Report—A Market Analysis and Forecast for Optoelectronics, Sensors/Actuators, and Discretes. The new 375-page report shows nothing stopping CMOS image sensors from continuing to set record-high annual sales and unit shipments through 2022 (Figure 1).  Figure 1 Figure 1TSMC Continues to Dominate the Worldwide Foundry MarketApril 24th, 2018 by IC Insights

only eight companies held 88% of global foundry market last year.

Research included in the recently released 50-page April Update to the 2018 edition of IC Insights’ McClean Report shows that in 2017, the top eight major foundry leaders (i.e., sales of ≥$1.0 billion) held 88% of the $62.3 billion worldwide foundry market (Figure 1). The 2017 share was the same level as in 2016 and one point higher than the share the top eight foundries represented in 2015. With the barriers to entry (e.g., fab costs, access to leading edge technology, etc.) into the foundry business being so high and rising, IC Insights expects this “major” marketshare figure to remain at or near this elevated level in the future.TSMC, by far, was the leader with $32.2 billion in sales last year. In fact, TSMC’s 2017 sales were over 5x that of second-ranked GlobalFoundries and more than 10x the sales of the fifth-ranked foundry SMIC.  Figure 1 Semiconductor Leaders’ Marketshares Surge Over the Past 10 YearsApril 11th, 2018 by IC Insights

Top 25 companies held more than three-fourths of worldwide semiconductor market.

Research included in the April Update to the 2018 edition of IC Insights’ McClean Report shows that the world’s leading semiconductor suppliers significantly increased their marketshare over the past decade. The top-5 semiconductor suppliers accounted for 43% of the world’s semiconductor sales in 2017, an increase of 10 percentage points from 10 years earlier (Figure 1). In total, the 2017 top-50 suppliers represented 88% of the total $444.7 billion worldwide semiconductor market last year, up 12 percentage points from the 76% share the top 50 companies held in 2007. U.S. Companies Maintain Largest Share of Fabless Company IC SalesMarch 22nd, 2018 by IC Insights

China-based companies show the largest fabless IC marketshare gain since 2010. Research included in the March Update to the 2018 edition of IC Insights’ McClean Report shows that fabless IC suppliers accounted for 27% of the world’s IC sales in 2017—an increase from 18% ten years earlier in 2007. As the name implies, fabless IC companies do not operate an IC fabrication facility of their own.Figure 1 shows the 2017 fabless company share of IC sales by company headquarters location. At 53%, U.S. companies accounted for the greatest share of fabless IC sales last year, although this share was down from 69% in 2010 (due in part to the acquisition of U.S.-based Broadcom by Singapore-based Avago). Broadcom Limited currently describes itself as a “co-headquartered” company with its headquarters in San Jose, California and Singapore, but it is in the process of establishing its headquarters entirely in the U.S. Once this takes place, the U.S. share of the fabless companies IC sales will again be about 69%.  Figure 1 Read the rest of U.S. Companies Maintain Largest Share of Fabless Company IC Sales IC Insights Raises 2018 IC Market Forecast from 8% to 15%March 14th, 2018 by IC Insights

Increased expectations for the DRAM and NAND flash markets spur upward revision.

IC Insights’ latest market, unit, and average selling price forecasts for 33 major IC product segments for 2018 through 2022 is included in the March Update to the 2018 McClean Report (MR18). The Update also includes an analysis of the major semiconductor suppliers’ capital spending plans for this year.The biggest adjustments to the original MR18 IC market forecasts were to the memory market; specifically the DRAM and NAND flash segments. The DRAM and NAND flash memory market growth forecasts for 2018 have been adjusted upward to 37% for DRAM (13% shown in MR18) and 17% for NAND flash (10% shown in MR18). The big increase in the DRAM market forecast for 2018 is primarily due to a much stronger ASP expected for this year than was originally forecast. IC Insights now forecasts that the DRAM ASP will register a 36% jump in 2018 as compared to 2017, when the DRAM ASP surged by an amazing 81%. Moreover, the NAND flash ASP is forecast to increase 10% this year, after jumping by 45% in 2017. In contrast to strong DRAM and NAND flash ASP increases, 2018 unit volume growth for these product segments is expected to be up only 1% and 6%, respectively. Read the rest of IC Insights Raises 2018 IC Market Forecast from 8% to 15% Are the Major DRAM Suppliers Stunting DRAM Demand?March 13th, 2018 by IC Insights

Skyrocketing DRAM prices potentially open the door for startup Chinese competitors. Historically, the DRAM market has been the most volatile of the major IC product segments. A good example of this was displayed over the past two years when the DRAM market declined 8% in 2016 only to surge by 77% in 2017! The March Update to the 2018 McClean Report (to be released later this month) will fully detail IC Insights’ latest forecast for the 2018 DRAM and total IC markets.In the 34-year period from 1978-2012, the DRAM price-per-bit declined by an average annual rate of 33%. However, from 2012 through 2017, the average DRAM price-per-bit decline was only 3% per year! Moreover, the 47% full-year 2017 jump in the price-per-bit of DRAM was the largest annual increase since 1978, surpassing the previous high of 45% registered 30 years ago in 1988!

In 2017, DRAM bit volume growth was 20%, half the 40% rate of increase registered in 2016. For 2018, each of the three major DRAM producers (e.g., Samsung, SK Hynix, and Micron) have stated that they expect DRAM bit volume growth to once again be about 20%. However, as shown in Figure 1, monthly year-over-year DRAM bit volume growth averaged only 13% over the nine-month period of May 2017 through January 2018. Figure 1 also plots the monthly price-per-Gb of DRAM from January of 2017 through January of 2018. As shown, the DRAM price-per-Gb has been on a steep rise, with prices being 47% higher in January 2018 as compared to one year earlier in January 2017. There is little doubt that electronic system manufacturers are currently scrambling to adjust and adapt to the skyrocketing cost of memory. 92 IC Wafer Fabs Closed or Repurposed From 2009-2017March 1st, 2018 by IC Insights

150mm and 200mm wafer fabs accounted for two-thirds of total closures.

Since the global economic recession of 2008-2009, the IC industry has been on a mission to pare down older capacity (i.e., ≤200mm wafers) in order to produce devices more cost-effectively on larger wafers. The spree of merger and acquisition activity and the migration to producing IC devices using sub-20nm process technology has also led suppliers to eliminate inefficient wafer fabs. From 2009-2017, semiconductor manufacturers around the world have closed or repurposed 92 wafer fabs, according to data compiled, updated, and now available in IC Insights’ Global Wafer Capacity 2018-2022 report. Figure 1 shows that since 2009, 41% of fab closures have been 150mm fabs and 26% have been 200mm wafer fabs. 300mm wafer fabs have accounted for only 10% of total fab closures since 2009. Qimonda was the first company to close a 300mm wafer fab after it went out of business in early 2009.  Figure 1 Read the rest of 92 IC Wafer Fabs Closed or Repurposed From 2009-2017 Integrated Circuit Technology Advances Continue to AmazeFebruary 21st, 2018 by IC Insights

Despite increasing costs of development, IC manufacturers are still making great strides. The success and proliferation of integrated circuits has largely hinged on the ability of IC manufacturers to continue offering more performance and functionality for the money. Driving down the cost of ICs (on a per-function or per-performance basis) is inescapably tied to a growing arsenal of technologies and wafer-fab manufacturing disciplines as mainstream CMOS processes reach their theoretical, practical, and economic limits. Among the many levers being pulled by IC designers and manufacturers are: feature-size reductions, introduction of new materials and transistor structures, migration to larger-diameter silicon wafers, higher throughput in fab equipment, increased factory automation, three-dimensional integration of circuitry and chips, and advanced IC packaging and holistic system-driven design approaches. For logic-oriented processes, companies are fabricating leading-edge devices such as high-performance microprocessors, low-power application processors, and other advanced logic devices using the 14nm and 10nm generations (Figure 1). There is more variety than ever among the processes companies offer, making it challenging to compare them in a fair and useful way. Moreover, “plus” or derivative versions of each process generation and half steps between major nodes have become regular occurrences. Top 10 Semiconductor R&D Spenders Increase Outlays 6% in 2017February 16th, 2018 by IC Insights

Intel far surpasses others with R&D spending of $13.1 billion in 2017 and accounts for 36% of expenditures among Top R&D spenders. The ten largest semiconductor R&D spenders increased their collective expenditures to $35.9 billion in 2017, an increase of 6% compared to $34.0 billion in 2016. Intel continued to far exceed all other semiconductor companies with R&D spending that reached $13.1 billion. In addition to representing 21.2% of its semiconductor sales last year, Intel’s R&D spending accounted for 36% of the top 10 R&D spending and about 22% of total worldwide semiconductor R&D expenditures of $58.9 billion in 2017, according to the 2018 edition of The McClean Report that was released in January 2018. Figure 1 shows IC Insights’ ranking of the top semiconductor R&D spenders, including both semiconductor manufacturers and fabless suppliers.

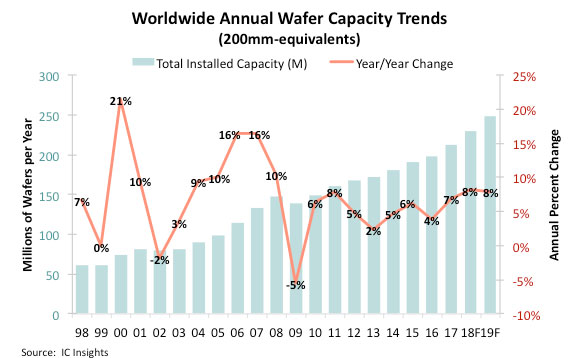

New IC Manufacturing Lines to Boost Total Industry Wafer Capacity 8%February 8th, 2018 by IC Insights

Wafer capacity growth of 8% forecast for 2018 and 2019 versus 4.8% average yearly growth from 2012-2017. IC industry wafer capacity, specifically in the memory segment, was inadequate to meet demand throughout 2017. However, with Samsung, SK Hynix, Micron, Intel, Toshiba/WD, and XMC/Yangtze River Storage Technology planning to significantly ramp up 3D NAND flash capacity over the next few years, and Samsung and SK Hynix boosting DRAM capacity this year and next, what does this mean for total industry capacity growth? In its 2018-2022 Global Wafer Capacity report, IC Insights shows that new manufacturing lines are expected to boost industry capacity 8% in both 2018 and 2019 (Figure 1). From 2017-2022, annual growth in IC industry capacity is forecast to average 6.0% compared to 4.8% average growth from 2012-2017.

Large swings in the addition or contraction of wafer capacity by the industry, as a whole, appear to be moderating. Since 2010, annual changes in wafer capacity volume have been in the relatively narrow range of 2-8%, with the largest year-to-year difference being just three percentage points. This suggests that IC manufacturers are better today than in years past about trying to match supply with demand. It’s still an incredibly difficult task for companies to gauge how much capacity will be needed to meet demand from customers, especially given the time it takes a company to move from the decision to build a new fab to that fab being ready for mass production. |

|

|

|||||

|

|

|||||

|

|||||

Animation, 3D Art and 3D Models")