Archive for the ‘Uncategorized’ Category

Tuesday, January 8th, 2019

Cryptocurrency boom in 1H18 helped China’s pure-play foundry market surge 41% last year.

IC Insights is in the process of completing its forecast and analysis of the IC industry and will present its new findings in The McClean Report 2019, which will be published later this month. Among the semiconductor industry data included in the new 400+ page report is an in-depth analysis of the IC foundry market and its suppliers.

With the recent rise of the fabless IC companies in China, the demand for foundry services has also risen in that country. In total, pure-play foundry sales in China jumped by 30% in 2017 to $7.6 billion, triple the 9% increase for the total pure-play foundry market that year. Moreover, in 2018, pure-play foundry sales to China surged by an amazing 41%, over 8x the 5% increase for the total pure-play foundry market last year.

(more…)

Tags: America, asia-, China, Europe, Forecast, foundry, Foundry Market, IC manufacturing, Japan, McClean Report, Semiconductors

No Comments »

Thursday, December 13th, 2018

DRAM fastest growing market in four of past six years, demonstrating very cyclical market.

IC Insights is in the process of revising its forecast and analysis of the IC industry and will present its new findings in The McClean Report 2019, which will be published in January 2019. Among the revisions is a complete update of forecast growth rates of the 33 main product categories classified by the World Semiconductor Trade Statistics organization (WSTS) through the year 2023.

Topping the chart of fastest-growing products for 2018 is DRAM, which comes as no surprise given the strong rise of average selling prices in this segment over the past two years (Figure 1). The 2018 DRAM market is expected to show an increase of 39%, a solid follow-up to the 77% growth in 2017. The number-one position is not unfamiliar territory for the DRAM market. It was also the fastest-growing IC segment in 2013 and 2014.

Figure 1

Figure 1

Remarkably, DRAM has been at the top and near the bottom of this list over the past six years, demonstrating its very volatile and cyclical nature. IC Insights forecasts that DRAM will rank nearly last in terms of market growth in 2019, with a 1% decrease in total sales. After two strong years of growth, Samsung, SK Hynix, and Micron—the world’s three primary DRAM suppliers—have expanded their manufacturing capacity and are beginning to ramp up production, bringing some much needed relief to strained supplies, especially for high-performance DRAM devices. At the same time, shipments of large-scale datacenter servers, which were a primary catalyst for much of the recent DRAM market surge, have begun to ease as uncertain economic and trade conditions factor into decisions about continuing with the strong build out.

NAND flash joins DRAM as another memory segment that has enjoyed very strong growth over the past two years (Figure 2). Solid-state computing, particularly, has been a key driver for high-density, high-performance NAND flash even as mobile applications continue to be a significant driver. Meanwhile, automotive and computing special purpose logic devices have also been strong performers the past two years. The top five IC markets listed for 2018 are the only product categories that are expected to surpasses the 17% growth rate of the total IC market this year.

Figure 2

Figure 2The full list of IC product rankings and forecasts for the 2019-2023 timeperiod is included in The McClean Report 2019, which will be released in January 2019.

Report Details: The 2019 McClean Report

The 2019 edition of The McClean Report—A Complete Analysis and Forecast of the Integrated Circuit Industry, will be released in January 2019. A subscription to The McClean Report includes free monthly updates from March through November (including a 200+ page Mid-Year Update), and free access to subscriber-only webinars throughout the year. An individual user license to the 2019 edition of The McClean Report is priced at $4,990 and includes an Internet access password. A multi-user worldwide corporate license is available for $7,990.

As part of your 2019 subscription, you are entitled to free attendance at a McClean Report seminar (one seat for each copy purchased; company-wide licensees receive five free seats). The schedule for next year’s McClean Report seminar tour is shown below.

Tuesday, January 22, 2019 — Scottsdale, Arizona

Thursday, January 24, 2019 — Sunnyvale, California

Tuesday, January 29, 2019 — Boston, Massachusetts

To review additional information about IC Insights’ new and existing market research reports and services please visit our website: www.icinsights.com.

More Information Contact

For more information regarding this Research Bulletin, please contact Bill McClean, President at IC Insights. Phone: +1-480-348-1133, email: bill@icinsights.com

Tags: automotive, DRAM, ICManufacturing, industrial, McClean Report, NAND, Semiconductors

No Comments »

Tuesday, May 8th, 2018

Embedded imaging applications in cars, security, machine vision, medical, virtual reality, and other new uses will offset slow growth in camera phones, says new report.

The spread of digital camera applications in vehicles, machine vision, human recognition and security systems, as well as for more powerful camera phones will drive CMOS image sensor sales to an eighth straight record-high level this year with worldwide revenues growing 10% to $13.7 billion, following a 19% surge in 2017, according to IC Insights’ 2018 O-S-D Report—A Market Analysis and Forecast for Optoelectronics, Sensors/Actuators, and Discretes. The new 375-page report shows nothing stopping CMOS image sensors from continuing to set record-high annual sales and unit shipments through 2022 (Figure 1).

Figure 1 Figure 1

Tags: automobile, camera phone, CMOS, hand-gesture interfaces, human recognition, Image Sensor, machine vision, medical\, Optoelectronics, security, virtual reality

No Comments »

Tuesday, April 24th, 2018

only eight companies held 88% of global foundry market last year.

Research included in the recently released 50-page April Update to the 2018 edition of IC Insights’ McClean Report shows that in 2017, the top eight major foundry leaders (i.e., sales of ≥$1.0 billion) held 88% of the $62.3 billion worldwide foundry market (Figure 1). The 2017 share was the same level as in 2016 and one point higher than the share the top eight foundries represented in 2015. With the barriers to entry (e.g., fab costs, access to leading edge technology, etc.) into the foundry business being so high and rising, IC Insights expects this “major” marketshare figure to remain at or near this elevated level in the future.TSMC, by far, was the leader with $32.2 billion in sales last year. In fact, TSMC’s 2017 sales were over 5x that of second-ranked GlobalFoundries and more than 10x the sales of the fifth-ranked foundry SMIC.

Figure 1

Figure 1

Tags: foundry, Foundry Market, globalfoundaries, huahong group, powerchip, samsung, Semiconductors, smic, tsmc, umc

No Comments »

Wednesday, April 11th, 2018

Top 25 companies held more than three-fourths of worldwide semiconductor market.

Research included in the April Update to the 2018 edition of IC Insights’ McClean Report shows that the world’s leading semiconductor suppliers significantly increased their marketshare over the past decade. The top-5 semiconductor suppliers accounted for 43% of the world’s semiconductor sales in 2017, an increase of 10 percentage points from 10 years earlier (Figure 1). In total, the 2017 top-50 suppliers represented 88% of the total $444.7 billion worldwide semiconductor market last year, up 12 percentage points from the 76% share the top 50 companies held in 2007.

Tags: IC, ICManufacturing, McClean Report, Semiconductors

No Comments »

Thursday, March 1st, 2018

150mm and 200mm wafer fabs accounted for two-thirds of total closures.

Since the global economic recession of 2008-2009, the IC industry has been on a mission to pare down older capacity (i.e., ≤200mm wafers) in order to produce devices more cost-effectively on larger wafers. The spree of merger and acquisition activity and the migration to producing IC devices using sub-20nm process technology has also led suppliers to eliminate inefficient wafer fabs. From 2009-2017, semiconductor manufacturers around the world have closed or repurposed 92 wafer fabs, according to data compiled, updated, and now available in IC Insights’ Global Wafer Capacity 2018-2022 report.

Figure 1 shows that since 2009, 41% of fab closures have been 150mm fabs and 26% have been 200mm wafer fabs. 300mm wafer fabs have accounted for only 10% of total fab closures since 2009. Qimonda was the first company to close a 300mm wafer fab after it went out of business in early 2009.

Figure 1

Figure 1 (more…)

Tags: Fab, wafer

No Comments »

Wednesday, February 21st, 2018

Despite increasing costs of development, IC manufacturers are still making great strides.

The success and proliferation of integrated circuits has largely hinged on the ability of IC manufacturers to continue offering more performance and functionality for the money. Driving down the cost of ICs (on a per-function or per-performance basis) is inescapably tied to a growing arsenal of technologies and wafer-fab manufacturing disciplines as mainstream CMOS processes reach their theoretical, practical, and economic limits. Among the many levers being pulled by IC designers and manufacturers are: feature-size reductions, introduction of new materials and transistor structures, migration to larger-diameter silicon wafers, higher throughput in fab equipment, increased factory automation, three-dimensional integration of circuitry and chips, and advanced IC packaging and holistic system-driven design approaches.

For logic-oriented processes, companies are fabricating leading-edge devices such as high-performance microprocessors, low-power application processors, and other advanced logic devices using the 14nm and 10nm generations (Figure 1). There is more variety than ever among the processes companies offer, making it challenging to compare them in a fair and useful way. Moreover, “plus” or derivative versions of each process generation and half steps between major nodes have become regular occurrences.

(more…)

Tags: IC, IC manufacturing, ICManufacturing, roadmap, Semiconductors, technology

No Comments »

Friday, February 16th, 2018

Intel far surpasses others with R&D spending of $13.1 billion in 2017 and accounts for 36% of expenditures among Top R&D spenders.

The ten largest semiconductor R&D spenders increased their collective expenditures to $35.9 billion in 2017, an increase of 6% compared to $34.0 billion in 2016. Intel continued to far exceed all other semiconductor companies with R&D spending that reached $13.1 billion. In addition to representing 21.2% of its semiconductor sales last year, Intel’s R&D spending accounted for 36% of the top 10 R&D spending and about 22% of total worldwide semiconductor R&D expenditures of $58.9 billion in 2017, according to the 2018 edition of The McClean Report that was released in January 2018. Figure 1 shows IC Insights’ ranking of the top semiconductor R&D spenders, including both semiconductor manufacturers and fabless suppliers.

Figure 1

Intel’s R&D expenditures increased just 3% in 2017, below its 8% average annual growth rate since 2001, according to the new report. Still, Intel’s R&D spending exceeded the combined R&D spending of the next four companies—Qualcomm, Broadcom, Samsung, and Toshiba—listed in the ranking.

(more…)

Tags: IC manufacturing, ICManufacturing, intel, qualcomm, r&d, Semiconductors, toshiba

No Comments »

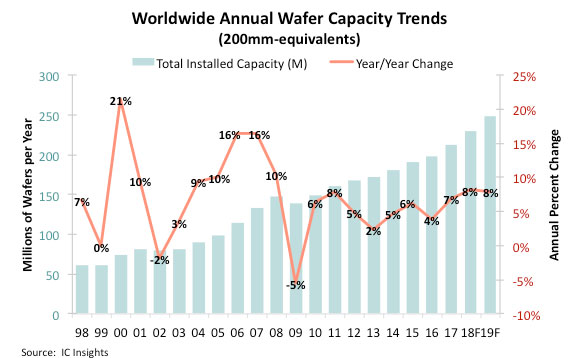

Thursday, February 8th, 2018

Wafer capacity growth of 8% forecast for 2018 and 2019 versus 4.8% average yearly growth from 2012-2017.

IC industry wafer capacity, specifically in the memory segment, was inadequate to meet demand throughout 2017. However, with Samsung, SK Hynix, Micron, Intel, Toshiba/WD, and XMC/Yangtze River Storage Technology planning to significantly ramp up 3D NAND flash capacity over the next few years, and Samsung and SK Hynix boosting DRAM capacity this year and next, what does this mean for total industry capacity growth? In its 2018-2022 Global Wafer Capacity report, IC Insights shows that new manufacturing lines are expected to boost industry capacity 8% in both 2018 and 2019 (Figure 1). From 2017-2022, annual growth in IC industry capacity is forecast to average 6.0% compared to 4.8% average growth from 2012-2017.

Figure 1

Large swings in the addition or contraction of wafer capacity by the industry, as a whole, appear to be moderating. Since 2010, annual changes in wafer capacity volume have been in the relatively narrow range of 2-8%, with the largest year-to-year difference being just three percentage points. This suggests that IC manufacturers are better today than in years past about trying to match supply with demand. It’s still an incredibly difficult task for companies to gauge how much capacity will be needed to meet demand from customers, especially given the time it takes a company to move from the decision to build a new fab to that fab being ready for mass production.

(more…)

Tags: IC manufacturing, ICManufacturing, Semiconductors, wafer

No Comments »

Thursday, February 1st, 2018

Though accounting for less than half of total MPU sales, data-handling cellphones, tablets, and MPUs for embedded processing applications to keep MPU market active through 2022.

Microprocessors, which first appeared in the early 1970s as 4-bit computing devices for calculators, are among the most complex integrated circuits on the market today. During the past four decades, powerful microprocessors have evolved into highly parallel multi-core 64-bit designs that contain all the functions of a computer’s central processing unit (CPU) as well as a growing number of system-level functions and accelerator blocks for graphics, video, and emerging artificial intelligence (AI) applications. MPUs are the “brains” of personal computers, servers, and large mainframes, but they can also be used for embedded processing in a wide range of systems, such as networking gear, computer peripherals, medical and industrial equipment, cars, televisions, set-top boxes, video-game consoles, wearable products and Internet of Things applications. The recently released 2018 edition of IC Insights’ McClean Report shows that the fastest growing types of microprocessors in the last five years have been mobile system-on-chip (SoC) designs for tablets and data-handling cellphones and MPUs used in embedded-processing applications (Figure 1).

Figure 1 Figure 1 (more…)

Tags: Acquisitions, AMD, chip, IC, Mergers, MobileSystem, MPU, Semiconductors

No Comments »

|

Animation, 3D Art and 3D Models")