As we saw last week in our special report on EDA startups, deep learning acceleration startups are more numerous and are getting much more funding. It’s therefore interesting to read the following comment by processor analyst Linley Gwennap: “Well-funded startups, including several unicorns, have been unable to demonstrate any advantage over Nvidia’s Ampere products, much less the upcoming Hopper generation. (…) Cerebras, Groq, and SambaNova, along with leading Chinese startups Enflame and Iluvatar, are in production but have published few or no benchmarks, probably owing to some combination of deficient hardware and unoptimized software. Of the best-funded AI-chip startups, only Graphcore has provided official MLPerf results, falling well short of Ampere in per-chip performance and power efficiency.” Let’s now move to this week’s news round-up, catching up on some of the updates from the last twenty days or so.

Cadence launches a computational fluid dynamics software suite

Cadence has recently introduced its Fidelity CFD Software, a suite of computational fluid dynamics solutions for multiple markets, including automotive, turbomachinery, marine, aerospace and others. The suite builds upon the expertise and technology that Cadence has gained from the Numeca and Pointwise acquisitions.

Despite the booming semiconductor industry, the number of new EDA startups is smaller than one would expect. Is the EDA industry’s status quo hindering innovation? Is venture capital overlooking EDA? We asked these and other questions to industry veterans (Lucio Lanza, Wally Rhines, Alberto Sangiovanni-Vincentelli) and startuppers (Chouki Aktouf, Keshav Amla)

“EDA, where electronics begins”: this was the title of a video produced in 2002 by the EDA Consortium (now Electronic System Design Alliance). The motto literally holds true today, in the so-called “semiconductor renaissance” era – an expression alluding not only to record high chip revenues and fab investments, but also to the dozens of startups developing new processing architectures for deep learning acceleration. In contrast, the number of new EDA startups seems to be smaller than one would expect. Undoubtedly, the current boom of the semiconductor industry is also benefitting the big EDA vendors and the EDA industry as a whole; just see the latest ESDA figures. Still, the relatively small number of EDA startups may raise some concerns, as these nascent companies are usually considered a key indicator of the liveliness and innovation capabilities of hi-tech industries. To shed some light on this matter, EDACafe talked to industry veterans and startuppers, getting interesting answers.

As the news from Ukraine gets more and more disturbing, the list of Western tech firm that have suspended business operations in Russia gets longer: among them, Intel. Before moving to this week’s tech news round-up, a quick mention of a market forecast concerning datacenters: according to market research firm TrendForce, the penetration rate of Arm architecture in datacenter servers will reach 22% by 2025.

Synopsys launches an EDA cloud SaaS solution

Synopsys has announced a new cloud-optimized EDA deployment model based on a single-source, pay-as-you-go approach. Called Synopsys Cloud, the service provides access to the company’s cloud-optimized design and verification products, with pre-optimized infrastructure on Microsoft Azure. The initiative aims at overcoming the limitations of conventional cloud-based EDA design, such as the difficulties in forecasting compute needs – leading to underestimation – or predefined design and verification capacity of the “bring your own cloud” (BYOC) approach. Synopsys is also working with major foundries to streamline access to required manufacturing collateral for use with its cloud-optimized products.

A few brief updates before moving to the rest of our weekly news round-up. Korean memory maker SK Hynix is reportedly considering the creation of a consortium to buy Arm. Speaking of memories, Apple is reportedly exploring alternative Flash suppliers for its iPhones, including China-based Yangtze Memory Technologies Co. Moving to the autonomous vehicle scenario, Waymohas started testing fully autonomous operations in San Francisco with Jaguar I-PACE electric cars. This new step comes after years of testing of fully autonomous service in the East Valley of Phoenix.

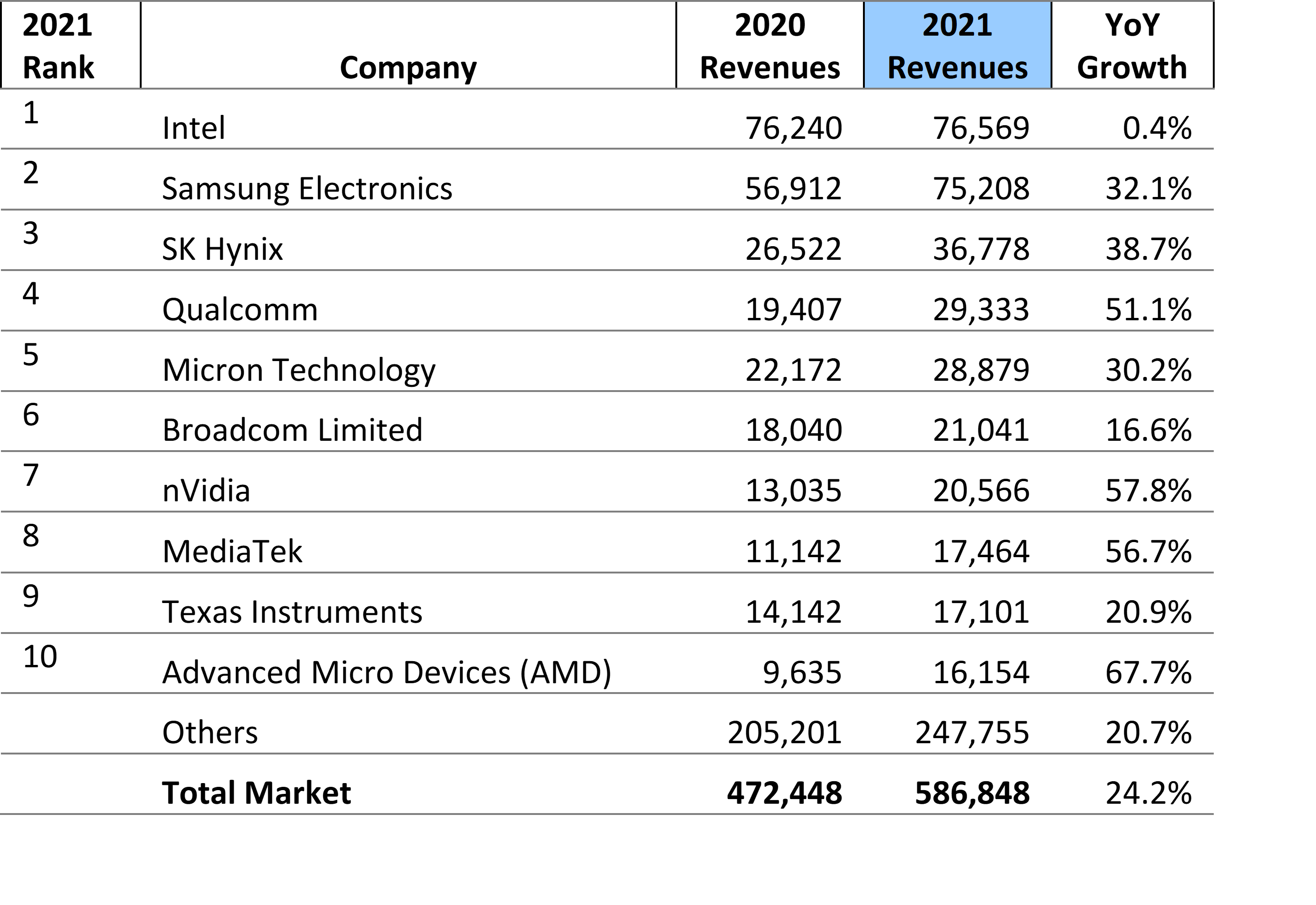

2021 semiconductor revenues

According to market research firm Omdia, the worldwide semiconductor market surpassed annual revenue of half-a-trillion dollars for the first time ever in 2021, and nearly 60% of companies in the sector grew by more than 20% in revenues. On an annual basis, Intel ranked as the number one semiconductor company in 2021, with revenue at $76.6B, which represented 13% of all semiconductor revenue for the year. Intel’s 2021 revenue growth was nearly flat from 2020, in contrast with the following top nine semiconductor firms which all experienced year-over-year growth above 15%. Omdia points out that the MPU product category – Intel’s core business – grew at just 11% YoY last year, much lower than the total semiconductor growth level of 24%. Samsung finished 2021 just behind Intel, with semiconductor revenue of $75.2B, representing 12.8% of all revenue for the industry. Samsung growth owes to the strong increase in the DRAM and NAND markets (up 42% and 23% respectively in 2021), as the Korean firm is the number one vendor for both product categories.

Animation, 3D Art and 3D Models")